When can the customer trust the financial advisor?

During the ongoing disease outbreak, the experts, authorities and well-intentioned peers flood the information channels. How do we know if the information is trustworthy and reliable? Most of us would not know and never know. Instead we trust by virtue of the labels that suggest expertise and official sources. Never mind that some opinions are more exaggerating than others.

Health care is an example of a credence good, characterized by deep informational asymmetries between the consumer, usually a layman, and the provider who is the expert. Typically, we trust the expert unless we have reason to believe otherwise. Financial advice falls in the same category as health care.

2 in 3 customers do not trust their advisor

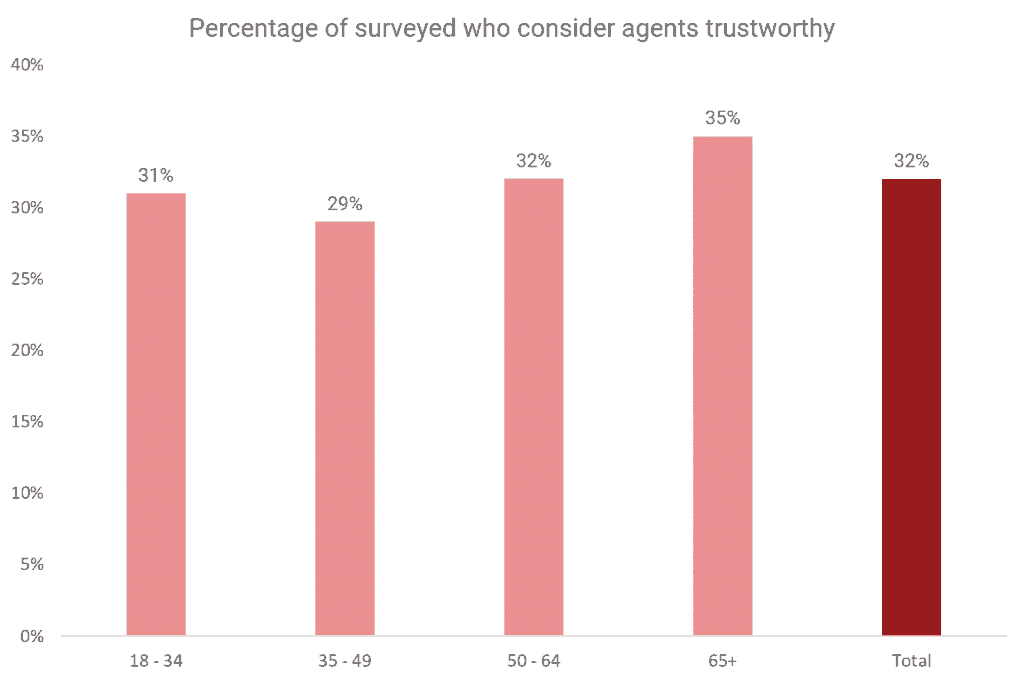

The consumers’ lack of trust in the financial advisor, presumably the expert, is consistent across investment and insurance. According to the Global Survey on the State of Investor Trust by CFA Institute in 2018, only 10% retail investors in Singapore and 7% in Hong Kong believe that their financial advisers always put their clients first. The global average was 35%. The Geneva Association 2018 Customer Survey showed only 32% surveyed across seven mature economies [1]

consider their agents trustworthy.

The lack of trust has many possible reasons. A commentary [2] by Andres Velasco summarizes the list well and applies to the financial advisory industry. The advisor may have good intentions to educate the need for life and health protection products or in fear of losing the prospect’s attention, commit the cardinal sin of hard selling a product upfront. The product jargon alone leaves a bad taste in the prospect’s mouth. Sometimes the prospect may even have had bad claims experience and relate it to bad advice. If the advisor gives the pronounced impression of biased motivation, distrust from the prospect deepens. Overall, if the prospect does not perceive that the advisor understands his or her own world, any advice will fall on deaf ears.

5000-customer-study shows gaps in advice quality

A recent 360F study highlights how the consumer’s distrust backfires on oneself.

In co-operation with a tier-1 insurer in a mature market, 360F ran its 360-FinHealthCheck® module to analyze financial planning and policy data points from 5,000 customers. Core findings include: (1) Incidence rate of overselling and mis-selling is insignificant, (2) The needs for investments and life protection are not systematically and holistically addressed. The siloed approach creates low needs fulfilment and (3) Needs fulfilment rate, while consistently low, differs largely even within sample clusters of similar affordability

From the customer’s perspective, his or her affordability has not been optimized to maximize his needs fulfilment. From the distributor’s perspective, there is a lot of room for cross- and upselling.

The low needs fulfilment rate can be easily attributed to the advisors’ technical competency, but trust plays a significant role. Unable or unconfident to win the prospect’s full trust, the advisor elicits too little information to truly understand his or her world. The advisor opts for an easy sale which frequently means proposing a small sum insured or regular savings that takes an insignificant portion of the prospect’s affordability but cannot cover the latter’s protection or retirement readiness gap.

An advisory autopilot for holistic, hyper-personalized and easy-to-evaluate financial advice

To win the prospect, the advisor must be able to demonstrate tangibly that his or her advice is trustworthy. The prospect must be able to understand and be understood.

360F’s advisory autopilot addresses these requirements. It captures the prospect’s profile in a mathematical function, expressing the financial happiness as uniquely defined by the individual. The autopilot then runs some 40 million rigorous simulations of personalized multi-risk & multi-year scenarios, including death, critical illness and even unemployment, to stress test the advisor’s proposed product(s) on the happiness function. The outcome is a score that indicates the impact of the advice on the prospect’s lifetime financial happiness. A series of indicators including forecast goal achievement and lifestyle sustainability is visible for the prospect and advisor to compare the effect of taking up the recommended product(s). This high level of transparency supported by an easy-to-understand journey enables the customer to not only make decisions confidently but also gain trust in the advisor.

Both the advisor and the prospect can compare, with statistical confidence, the impact of advice and product(s) on the latter’s lifetime needs and wants

The 360F advisory autopilot enables my clients and I to have enjoyable and productive discussions. Instead of handling objections, I get to discuss with my clients the engine-generated solution, and can show them instantly the impact of their preferences on their holistic financial outcome. As the recommendations have been exhaustively stress-tested, my clients feel assured to make their purchase decisions swiftly.”

Asfar Ibrahim, Advisory Manager, Zurich Insurance Distribution Partner

Closing the protection and retirement readiness gaps

In this day and age, consumers are aware that they have financial gaps, and they want to participate in the solutioning process. While they may struggle to understand product jargon, they will not take advice on blind faith in the expert. Helping consumers understand the tangible impact of financial advice, indirectly enabling advice quality to be scored objectively and therefore trust in the advisor to increase, may well be the breakthrough that nations worldwide need to close the protection and retirement readiness gaps.

Want to discuss more? Drop us an eMail here: clarie.kwa@360f.com

Notes

[1] United States, the United Kingdom, France, Germany, Italy, Japan and Switzerland

[2] “If experts know so much, why don’t people trust them?” Source: Business Times, Jun 2019