Sprint → Stall → Rebuild

2019–2024

- Bancassurance whiplash: Hyper-growth without appropriate customer knowledge met consumer pushback; early lapses exposed mis-aligned incentives.

- Boom to Bust: New business premiums soared 24% in 2019.

- Regulators stepped in: Forced tie-ins banned; suitability, disclosures, and cool-off periods sharpened; sales shifted from push to purpose.

The Reset in Motion

2024–2025

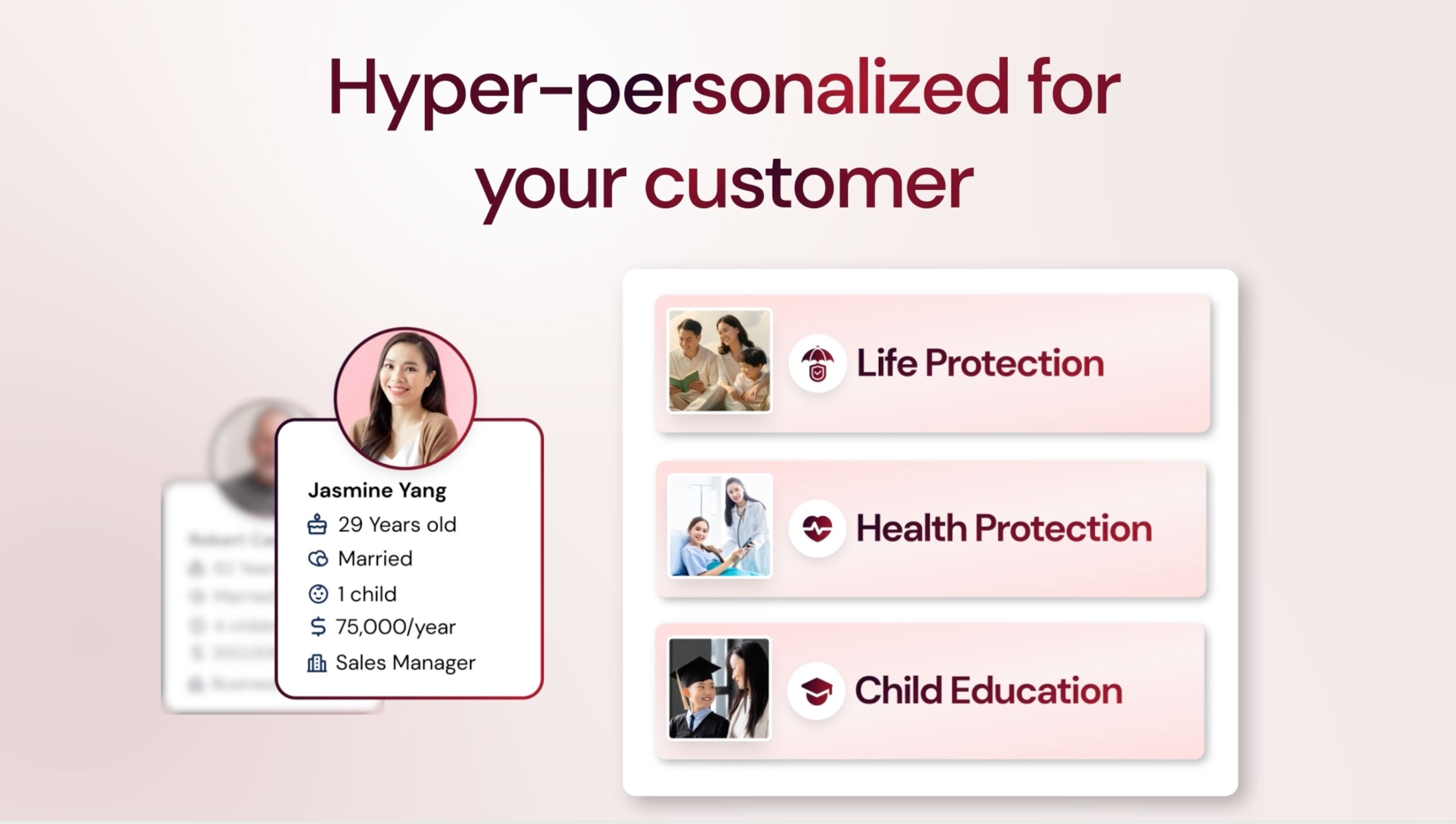

- Products redesigned for clarity: Complex ILPs pulled back; universal life and term policies re-launched with modular riders. Fewer moving parts → easier for customers to understand, harder to mis-sell.

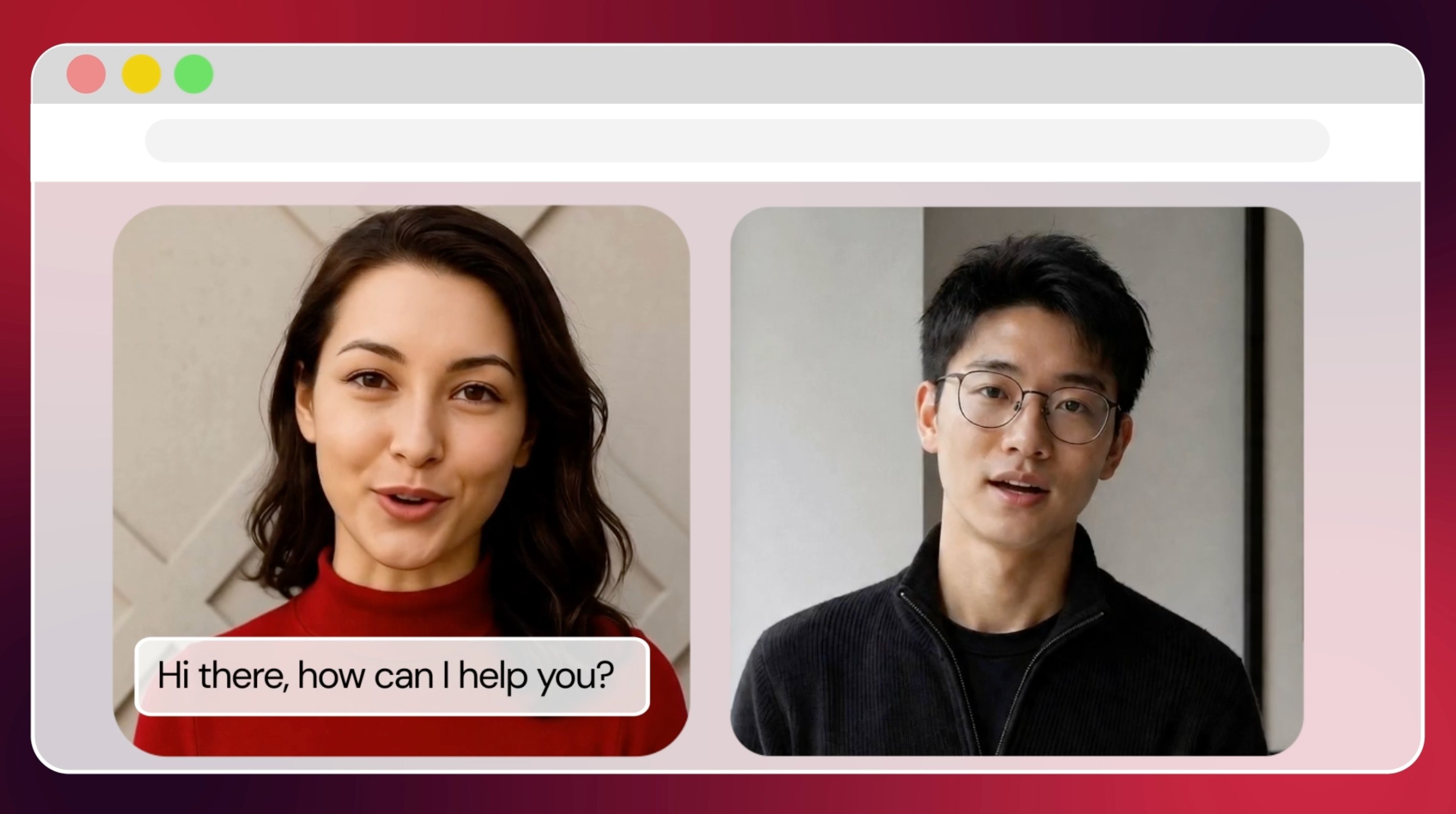

- Tech at the core of service: Digital submissions, voice-recorded customer consent became the new normal. Instant feedback loops and increase in free look period.

Bancassurance, Right-Sized

Distribution & Product Remix

The bancassurance model in Vietnam is being recalibrated not dismantled. Banks and insurers are renegotiating partnerships around quality metrics rather than raw volume, creating incentive structures that better align with long-term customer outcomes. New digital-first distribution models are complementing the bank channel rather than replacing it.

The Start of a New Growth Cycle

Why We're Optimistic

Vietnam's fundamentals remain compelling: a young population, rising middle class, and chronically low insurance penetration rates. The regulatory reset has created the conditions for sustainable, trust-based growth. Consumers who previously felt burned are showing renewed openness to protection products on their terms.

This reset isn't just cleanup it's the start of a new growth cycle. Who else is optimistic about Vietnam's insurance future?